While I’m not a professional money manager, I want to publicize my portfolio and returns for a couple reasons:

- Portfolios reflect people’s biases and how they see the world.

- Theory is indispensable, but putting it into practice is what matters.

- If I want to eventually manage other people’s money like I manage my own, it provides greater transparency, accountability, and credibility.

Disclosure: Nothing on this site should be taken as investment advice. Positions I hold reflect my views at a given time and can change without notice. Investing is subjective and you cannot borrow conviction.

To compound wealth requires patience, emotional stability, and a long-term perspective. My turnover is therefore pretty low. I prefer inaction to action, though inaction is in a way, action. I’ll make more errors of omission than commission, but will commit plenty of the latter. Staying grounded in your process makes decisions much easier to live with, right or wrong. Because new information causes constant fluctuations in value and price, filtering through the noise with skepticism, humility, and mental models is critical. My circle of competence is small, but steadily growing. I read widely, and sometimes get overwhelmed by how much I don’t know, even about the businesses I own!

As I’ve gained more experience, my thinking has morphed from “this stock is cheap and should go up” to “this company is potentially undervalued if they maintain their competitive advantage and demand grows alongside value-add.” I’d argue, without any evidence, that investors cap out at 80% confidence in an investment. By “confidence” I mean shoving all your chips into the pot knowing you’ll win. Because for one, the future holds irreducible uncertainties. And two, Mr. Market is unlikely to offer the low prices that he has historically due to the exponential increase in information, skill, and capital needing to be put to work.

I do not have a concrete methodology for position sizing; it is purely based on conviction. My conviction is based on my estimate of the gap between price and value, my probabilistic discounting of future outcomes, and my assessment of the business’ durability, adaptability, and optionality. Similar to other value investors, I more heavily weigh the potential downside than upside; meaning, I focus more on what I could lose than on generating super returns. Buffett’s two rules of investing come to mind.

It goes without saying that both skill and luck influence returns. Skill encompasses buying companies for less than they’re worth, holding during price fluctuations if your thesis remains intact, and reallocating elsewhere if better opportunities arise. Luck encompasses near-term price movements and unforeseeable events. Therefore, investment managers should be judged over multiple years and cycles, not over months during one part of a cycle. To me, risk is inherent to the investment, and is thus permanent loss of capital caused by buying at a price higher than the business’ value, as opposed to volatility, which is simply the market’s evolving perception of value.

Portfolios are always a work in progress, and mine is far from perfect. The goal is to buy and hold quality businesses that offer an attractive risk-adjusted return at their current market valuation. Arguments for and against any one stock are plentiful, so understanding human biases and evaluating disconfirming evidence are critical to forming the most accurate view of the world as possible. All we can do is get a little smarter every day.

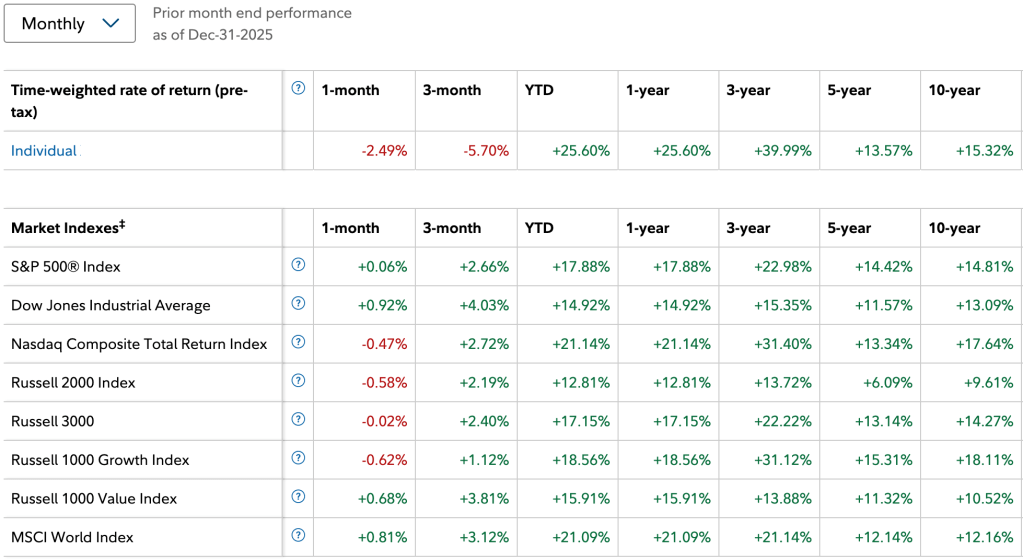

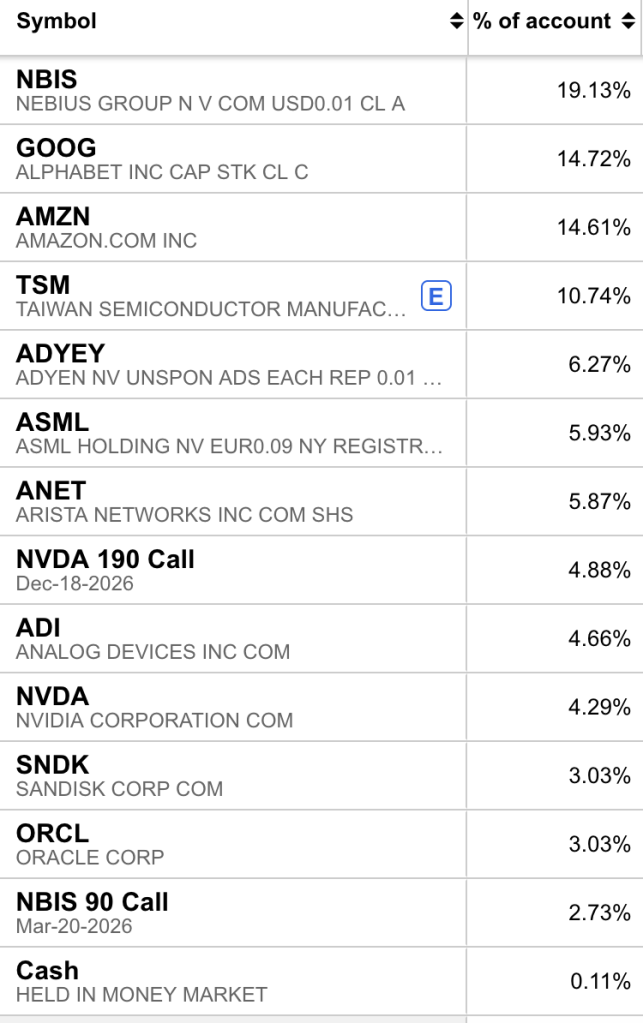

I will update my holdings and returns monthly.