I try to be more knowledgeable each year as an investor.

Sir John Templeton

2022 was brutal. Inflation was rampant, consumers were pinched, and risk assets fell precipitously. Even crypto had a reckoning (gasp!). The standouts were commodities and the US dollar – what a strange combination. It was certainly a terrible year for “high-growth, valuation-agnostic” investors as the high-flyers of previous years came crashing down. Although I don’t classify myself as a this type of investor, I do hold many stocks that are high-growth and highly valued, which means I wasn’t spared from the carnage!

In this post, I’m going to reflect on the year and conclude with some takeaways for myself. I write mostly for my present and future self, but if there is something that you dear reader learn or helps you think more critically, that’s a cherry on top.

As happens after bad performance, I’ve seen many post-mortems, cataloging of mistakes, and revisiting of processes by investors attempting to prevent future catastrophic drawdowns. I’ve also seen a lot of shade thrown at professional investors who were down big. I think dancing on graves isn’t particularly admirable, although it depends on the grave. It’s fine to celebrate the downfall of the grifters, shameless promotors, and Ponzi architects. But I take issue with dunking on professional portfolio managers whose positions got swept up in the prior mania. Those criticizing almost certainly felt a little envy during the previous years, so when the tide turned they were quick to jump on the “what an idiot!” train. That said, they may not be wrong, but there’s plenty of room for humility and nuance.

Much of the criticisms and mea-culpas are presented under the guise of “risk management.” Meaning, investors who did poorly in 2022 didn’t pay enough attention to the risk they were taking (i.e. the one way factor bet or the correlations between their holdings) or that they should’ve sold stocks when the market was falling and interest rates were rising (i.e. implement stop losses to prevent downside). But in my opinion, the year for “risk management” was 2021. Why? Because risk is the highest when it appears the lowest. The most dangerous moments are when everything is going swimmingly because your guard is down; you’re unprepared for the unexpected. See how Houdini died or when catastrophic failures occur.

A common question in 2021 was, “does valuation matter?” Stocks that were highly valued on trailing fundamentals but were growing fast simply kept going up. Underlying FOMO became justification for “I look at valuation last.” Another prominent refrain (and hashtag) was “#neversell” in terms of using a simple buy and hold (or hodl) strategy because stocks “only go up.” Citing the history of Amazon, Netflix, Salesforce or similarly “always expensive” compounders, many investors focused more on revenue growth and TAM while ignoring current earnings or free cash flow. Not to mention the prices that certain JPEGs received.

In hindsight, this was silly and a clear indicator of investor euphoria. But at the time, cogent arguments were presented that seemingly justified a new paradigm coming out of covid. Counterintuitively, consumers and businesses were flush with cash, aided by government and Federal Reserve stimulus, and they were willing to spend. In 2021, US Real GDP grew 5.72%, the highest since the early 80s. Remember “revenge spending”? That was fun. The constraint, was supply; notably for labor. Adding in the low interest rate environment, stock prices were driven higher.

Of course, times change. Therein lies the risk in investing. Predictable can become unpredictable (e.g. input costs, supply chains, “recurring” revenue). Strengths can become weaknesses (e.g. operating leverage, stock based compensation, capex). A “justifiable” price can become “unjustifiable” when a new environment prevails. And in 2021, many stocks were being priced for perfection.

To illustrate why price matters, imagine a magical box that randomly spit out between $1 and $5 every day. The catch is that it runs on a non-rechargeable battery, and nobody knows how long the battery will last. How much would you pay to own said box? Some would pay no more than $5, while others may pay up to $20. Or $100. Or $200. Those who are willing to pay a higher price must be optimistic that the battery will last a long time.

Now, imagine there became an obsession with these rare magical boxes. They were all over the news. People that owned them held some status. “It literally gives you free money every day!” The price for these boxes increased, but the underlying fundamentals remained the same. Furthermore, some dishonest people might start selling fake boxes, proclaiming that this one could spit out up to $10. Who could know if a $10 just hadn’t come out yet!

Although this is a crude and simplistic analogy, the point is that the price paid for the box could turn out to be splendid if the box operates for a long time and you paid a relatively low price. Or the box could fail tomorrow and you overpaid. What’s more, is that the market determines the current price of the box while you can only determine the price you pay. Maybe you paid a low price initially, but now the boxes are worth a lot more. Should you sell it to an enthusiastic buyer? Or look to the status you’ve gained and prefer to hold on to it. Besides, you kind of enjoy having a magical box that spits out free money, and there’s been many $5 lately! A predicament indeed.

Takeaway #1

Valuation, in terms of the price I pay as well as the prevailing market price, ALWAYS matters. Over time, stocks will converge to the business’ intrinsic value, but the rate of return from any point in time differs depending on the price. A great business does not always make a great investment. Investing is all about a comparison between value and price. The rate of return is generally predicated on the growth in earnings/cash flows and prevailing price. In all of the great investors’ description of their processes, “at an attractive price” is always expressed. If you’ve seen otherwise, please let me know. The difficulty is delineating what an attractive price is, and importantly, what to do (or not do) in the absence of attractive prices. Patience, is a virtue.

Takeaway #2

I should #neversell UNLESS the price is vastly above my estimate of the business’ intrinsic value. In some cases, holding quality businesses – which is what I aim for – will turn out just fine. But, tying up capital in an idea rather than redeploying it brings about opportunity cost, which will eat into returns. I will never implement stop losses since that is for traders, nor will I sell purely based on price movements. It’s crucial to maintain a business owner’s mindset. But, I must realize there is an opportunity to take advantage of stupidity in markets. I should have trimmed more when I believed the forward rate of return was low, in the same way I was eager to buy when the reverse is the case. Trying to time the market almost always turns out to be a mistake, but I should be better at anticipating revisions to expectations. And remember, “People mistake timing the market for assessing value because they are often indistinguishable, especially externally. Key is to know the difference internally, and to not fool yourself.”

Obviously, investors who did poorly in 2022 chose not to sell on the way down, either. With a large dose of hindsight, of course this was a “mistake.” However, for a lot of fund managers who share a similar philosophy of being a long-only, value driven, and macro-agnostic, the inclination is to hold through volatility driven by exogenous factors. The benefits of this approach are widely recognized. The main drawback is that short term volatility will be fully felt. This is where you must be brutally honest in knowing yourself and your “risk” tolerance.

Takeaway #3

I should continue to be macro-agnostic, BUT be more macro-aware, because the economic environment does impact intrinsic values. Being macro-agnostic doesn’t mean don’t pay any attention to what’s going on with the economy. It means not ascribing much weight in macro forecasts. However, in the same way that stimulus helped people and businesses through covid, certain policies and economic developments can change the trajectory of business fundamentals. How new developments impact the probabilities going forward must be taken into account. Predicting the economy or inflation is a fool’s errand. But even a fool should’ve seen that 8% inflation and a 1% Fed Funds rate are incongruent. Interest rates are fundamental to asset prices.

Takeaway #4

I should be even more vigilant to not get caught up in the market sentiment. Controlling your emotions is the hardest part of investing, especially during prolonged volatility, to the upside and downside. Markets test your brain and gut. Riding an uptrend in “beat and raises” is fun. Riding a downtrend is depressing. Don’t become overconfident. Don’t become despondent. Avoid jealousy and comparison since you do not live anybody else’s life but your own. Be contrarian, but realize when you’re not actually contrarian.

The role of a portfolio manager is to make intelligent investment decisions. Unfortunately, investment decisions that are inherently long-term in nature are judged over the short run. Different portfolio managers have different styles based on their personality and “circle of competence,” but the goal is the same: generate a high rate of return.

In March 2021, I tweeted “If Cathie Wood were the next Buffett, she’d be closing down shop and returning money to investors.”

I was referencing the fact that Buffett closed his partnership in 1969 after achieving a 12 year annual compound return of ~25%(!) writing, “I am not attuned to this market environment and I don’t want to spoil a decent record by trying to play a game I don’t understand just so I can go out a hero.” Legendary. Yet another example of why he is the GOAT, and why it’s silly to think others even come close.

If investing is a game, portfolio returns are the scoreboard. But in investing, there is no final buzzer. No handshakes or “we’ll get it next time.” No starting over. Sure, a new year provides a blank slate for YTD returns. But the track record since inception is continual, which is where the great investors distance themselves from the rest. Fortunately, my professional starting clock has yet to begin.

Takeaway #5

Attract clients that will stick with you through the trying times, professionally and personally, by ALWAYS acting in a high-quality manner. In the same way mean reversion can equilibrate prices over time, underperformance will follow outperformance. Establish meaningful relationships with your clients by acting with humility and integrity. Avoid permanent capital destruction and mental rigidity. Always be realistic regarding expectations about returns and your knowledge.

Although I was already aware of these “lessons,” 2022 was unfortunately a powerful reminder. Note that none of these takeaways are related to becoming smarter with regard to the Fed or inflation. They are about improving my process and behavior. The key is the nuance within each and to not over-apply what would have prevented the underperformance. 2022 was a unique year where the macro took over, and both fundamentals and the discount rate worked against risk assets.

I went back to read what I wrote during the 2020 crash and found that I had a similar, though much more stoic demeanor.

Losing money is obviously painful, but volatility is the price of admission. There’s a strong possibility I have a screw loose because I rather enjoy it; it’s exciting. How often do companies lose 50% or more of their market value in three weeks? Like Buffett says, if you’re a net buyer of stocks over the long-term you should cheer for price declines so you can buy them on sale. The difficulty, as always, is figuring out what actually is on sale.

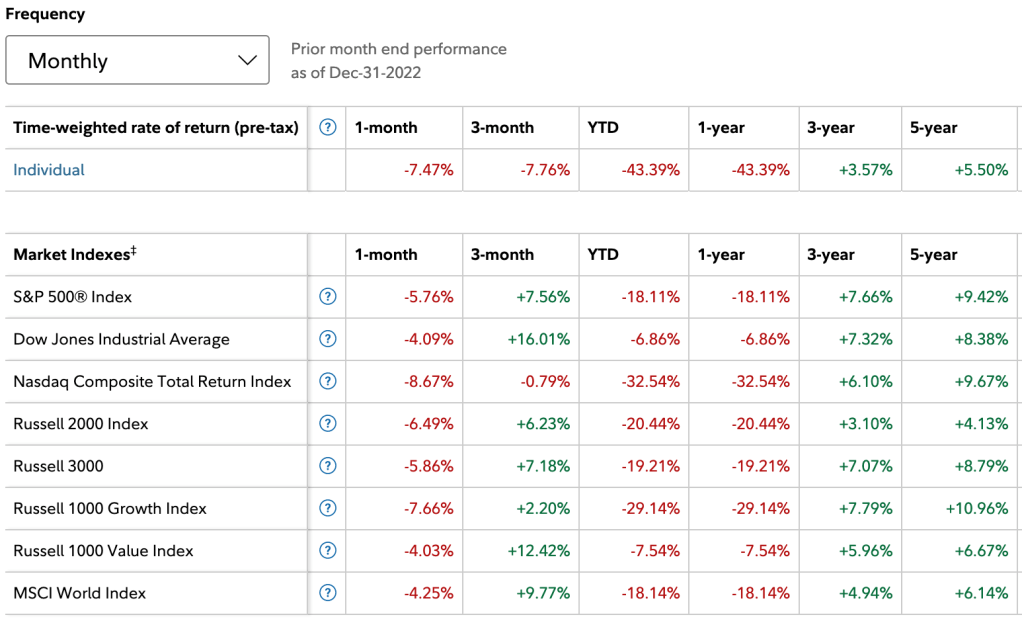

My current thoughts and the below screenshot will be quite interesting to look back on in 3 years. My portfolio will have to outperform dramatically to claw back the large underperformance. But I’m more determined than ever. Declaring so doesn’t mean using leverage (never have) or trading more actively (I’m a terrible trader). It means doubling down on the depth of my analysis about the companies I own and leaning even more into my convictions. In some cases, it also means admitting I should not have had as strong of a conviction as I did!

Investors must always learn and adapt, which makes the game so addicting. There are very few businesses that become outsized winners. Choose wisely, and know you’ll often be wrong.